Personal finance can be made to seem quite complicated, but really it comes down to two things:

- Helping clients save money

- What you, as an advisor, do with that saved money to grow their wealth

Starting out as a new advisor most people begin with either the life insurance side or the investment side. I had some investment knowledge that I expanded on and learned about life insurance as a foundational piece of a financial strategy.However, over time I realized that if I wanted to be clients’ “go to” holistic financial guy I would need to become familiar with products and ideas that I did not sell and wasn’t directly involved with implementing. This included property & casualty insurance, social security, legal documents, banking, retirement plans, managed money, loans, accounting, real estate, and small businesses. So, I did this. I learned about these areas and developed relationships with specialists in these fields. I wasn’t aware of this at this time, but it became apparent that cash flow was maybe the most important area because it is the resource used to fund all these other things. To be successful, I knew I needed to help my clients understand cash flow.

As we were taught, money is a scarce commodity and there is only so much to go around. At some point the financial philosophy I followed (Leap) expanded its model to integrate debt and cash flow for financial success. Phase I was to clean up someone’s current financial model/situation and phase II was ongoing future moves and structure. The biggest part of this was helping clients direct cash flow. I loved this idea. It made sense. I had never encountered a real attempt to solve this issue.

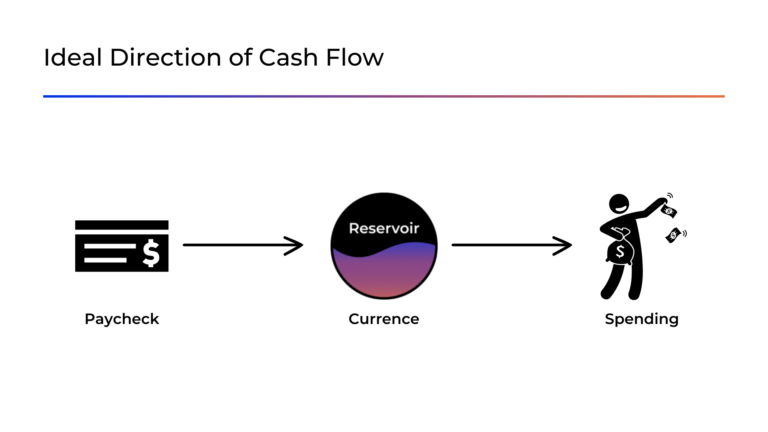

Leap focuses on the Wealth Coordination Account (WCA), a bank account that is the hub between earnings and spending to control and track consumption and wealth building. It segregates money in pristine accounts so these different areas were not comingled which enables them to be tracked without rigid budgeting. I thought the concept was genius. It became clear when people separated their money in this way they became better savers.

Putting this idea into practice was difficult for many reasons. One was that I had to send my clients off to their retail bank to open the accounts, and I didn’t have purview into the account. The best we could do was a brokerage account, and this had limitations with functionality, portability, and was not ideal. Another main issue was that clients were off living their lives and I was living mine, so we weren’t really connected, which makes accuracy and consistency difficult. This made it clunky and quite a bit of work. Because of this I didn’t really follow through as much as I should have or wanted to be effective. I would bring it up with clients but didn’t push that hard for implementation. To be honest, I even felt somewhat relieved at times when clients didn’t want to pursue help with their cash flow. I knew I was glossing over a very important aspect of their financial lives. I knew there was a hole in my practice, and I knew there was no one in the marketplace filling this void. I had guilt that I was essentially ignoring this imperative piece of clients’ financial lives – cash flow.

Fast forward to the covid lockdowns. Everything becomes an unknown and many peoples’ livelihoods are changed, and finances are altered. Some were more prepared than others. Seeking human interaction and face to face collaboration, my first post-COVID industry conference was a two-day event in Southlake, Texas to see Bob Castiglione speak. I hadn’t seen him speak in quite some time and have been following his philosophy for twenty years.

A great re-orientation to in-person events, I enjoyed listening to Bob for a day and a half, but one of my biggest takeaways was at the very end. It was around two o’clock and Bob had already left. I had a 5pm flight and was checked out of my hotel room and half-checked out of the conference thinking about an Uber to the airport when the final guest speaker was introduced. It was Dave Mozeika and later Vince D’Addona. I had been to several of Vince’s speaking events previously over the years and knew a little about Dave.

Dave introduced the audience to Currence. He told us his entire background story, and how it became a struggle implementing wealth coordination accounts manually to handle his clients’ cash flow. He searched for a solution that already existed within the marketplace, but only found ineffective budgeting apps – and people hate budgeting. Dave shared how frustrated he became because it was so much work and taking up too much of his time. He couldn’t scale. This was my experience as well. But Dave did something about it, he took the initiative to build something that didn’t exist to solve a major financial problem – I was impressed.

I then realized that they built an app that is essentially an automated WCA with additional functionality, so it is even better than the original idea that I already loved. I went from checked-out to completely engaged – my mind spinning with ideas. As I investigated further and attended the next Currence symposium in Nashville, I signed up as a user myself. It truly is a game changer that exists nowhere else in the industry. It was the missing piece – filling a huge void in my practice. Now, I am confident I can assist clients in any area of their financial lives and have the tools to do so effectively. Currence removed the barrier to me becoming a cash flow expert for my clients.

About the Author

Robert Bockel

For the past 18 years, Robert has been consulting with physicians & dental specialists to help position all of the pieces of their financial puzzle together properly with their professional and personal planning. In an industry that segregates business finance and personal finance Robert integrates the two and becomes the resource who can bridge the two together. These areas are intimately related – the more efficient we are with our professional time and profitability the sooner we can slow down and enjoy our personal time and other endeavors. The risk is that we make some partial financial decisions in our thirties and in a flash we are in fifties with less of our most valuable asset – time. It is important to have strategies in place with contingencies so we are not forced to work beyond our desired time and have dreams put on hold. Robert looks to become a trusted resource in the lives of medical and dental specialists so these areas of their financial lives can be coordinated with his specialists and their other advisors. The decision to work within the medical & dental space was impacted by his father who was a successful radiologist for 40 years. Robert is able to make a significant impact in these professionals’ lives without having to completely overhaul good work that has been put in place.

This content is for general, informational purposes only. You should not interpret any such information – including referenced or attached materials – as legal, tax, investment, financial, or other professional advice. Please consult a qualified financial, tax, or legal professional for advice specific to your situation.